Chapter 3.78

MULTIFAMILY PROPERTY TAX EXEMPTION

Sections:

3.78.040 TERMS OF THE TAX EXEMPTION.

3.78.060 APPLICATION PROCEDURE.

3.78.070 APPLICATION FOR CONDITIONAL CERTIFICATE.

3.78.080 EXTENSION OF CONDITIONAL CERTIFICATE.

3.78.090 APPLICATION FOR FINAL CERTIFICATE.

3.78.100 ISSUANCE OF FINAL CERTIFICATE.

3.78.105 AFFORDABLE HOUSING CAPITAL FUND.

3.78.110 ANNUAL COMPLIANCE REVIEW.

3.78.120 CANCELLATION OF TAX EXEMPTION.

3.78.130 CONFLICT OF PROVISIONS.

3.78.140 EXTENSION OF TAX EXEMPTION.

3.78.010 PURPOSE.

As provided for in Chapter 84.14 RCW, the purpose of this chapter is to provide limited exemptions from ad valorem property taxation for multifamily housing in designated residential targeted areas to:

(a) Encourage increased residential opportunities, including affordable housing units, within areas of the City designated by the City Council as residential targeted areas; and/or

(b) Stimulate new construction or rehabilitation of existing vacant and underutilized buildings for multifamily housing in designated residential targeted areas to increase and improve housing opportunities, including affordable housing; and

(c) Assist in directing future population growth to designated residential targeted areas, thereby reducing development pressure on single-family residential neighborhoods; and

(d) Achieve development densities which are more conducive to transit use in designated residential targeted areas. (Ord. 5463 §2, 2022; Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.020 DEFINITIONS.

When used in this chapter, the following terms shall have the following meanings, unless the context indicates otherwise:

(a) "Affordable housing" means residential housing that is rented by a person or household whose monthly housing costs, including utilities other than telephone, do not exceed thirty (30) percent of the household’s monthly income. For the purposes of housing intended for owner occupancy, "affordable housing" means residential housing that is within the means of low- or moderate-income households.

(b) "Building codes" means the City and state building and fire codes as set forth in Chapters 17.04, 18.02 and 18.03 BMC.

(c) "City" means the City of Bremerton.

(d) "Department" means the City Department of Community Development.

(e) "Director" means the Director of the Department of Community Development, or designee.

(f) "Household" means a single person, family, or unrelated persons living together.

(g) "Low-income household" means a single person, family, or unrelated persons living together whose adjusted income is at or below eighty (80) percent of the median family income adjusted for family size, for the county where the project is located, as reported by the United States Department of Housing and Urban Development.

(h) "Moderate-income household" means a single person, family, or unrelated persons living together whose adjusted income is more than eighty (80) percent but is at or below one hundred fifteen (115) percent of the median family income adjusted for family size, for the county where the project is located, as reported by the United States Department of Housing and Urban Development. For cities located in high-cost areas, "moderate-income household" means a household that has an income that is more than one hundred (100) percent, but at or below one hundred fifty (150) percent, of the median family income adjusted for family size, for the county where the project is located.

(i) "Multifamily housing" means a building having ten (10) or more dwelling units not designed or used as transient accommodations and not including hotels and motels. Multifamily units may result from new construction or rehabilitated or conversion of vacant, underutilized, or substandard buildings to multifamily housing.

(j) "Multifamily property tax exemption" means an exemption from ad valorem property taxation for multifamily housing.

(k) "Owner" means the property owner of record.

(l) "Permanent residential occupancy" means multiunit housing that provides either rental or owner occupancy on a nontransient basis. This includes owner-occupied or rental accommodation that is leased for a period of at least one (1) month. This excludes hotels and motels that predominantly offer rental accommodation on a daily or weekly basis.

(m) "Rehabilitation improvements" means modifications to existing structures that are vacant for twelve (12) months or longer that are made to achieve a condition of substantial compliance with existing building, fire, and zoning codes, or modification to existing occupied structures which increase the number of multifamily housing units.

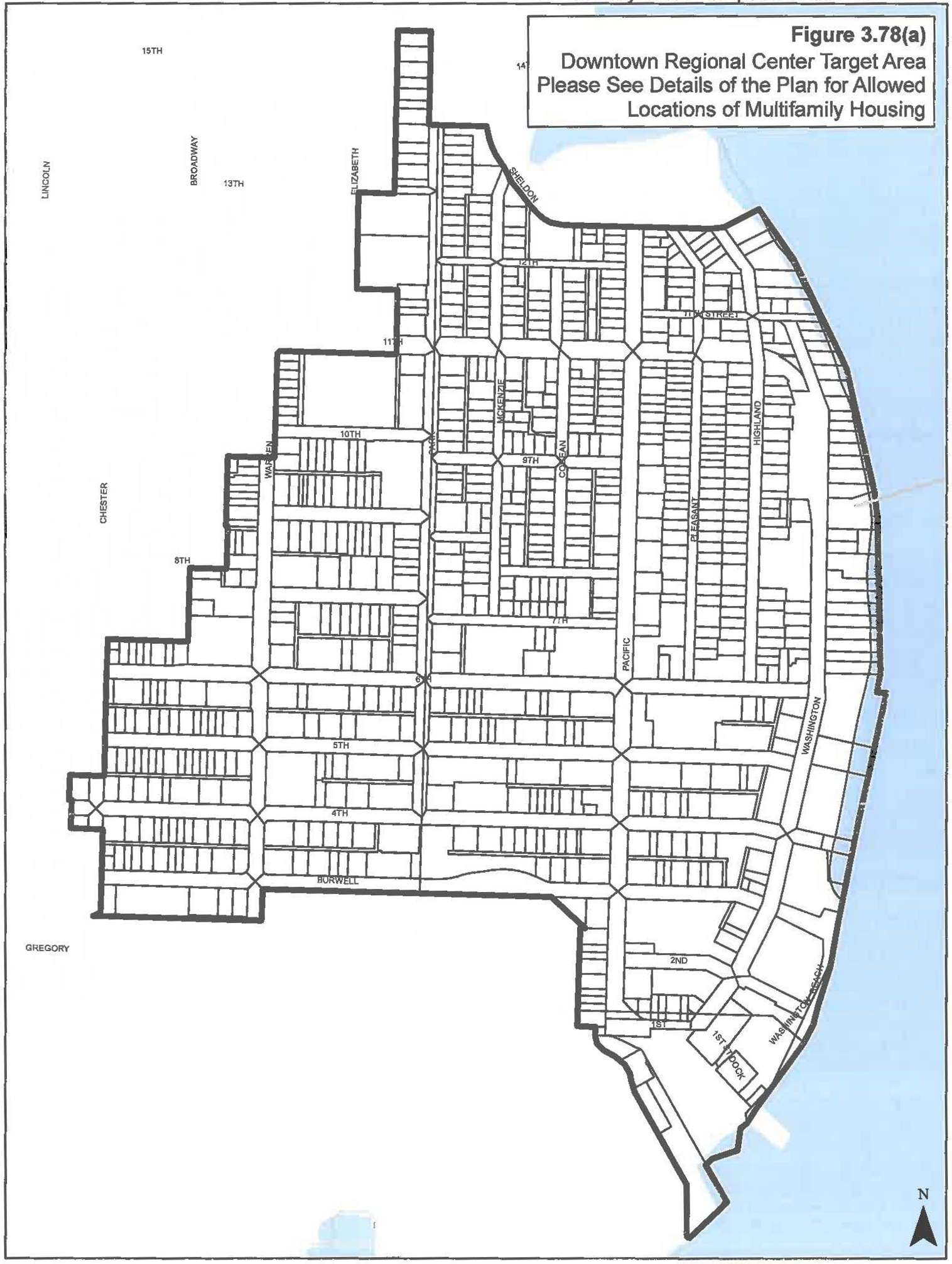

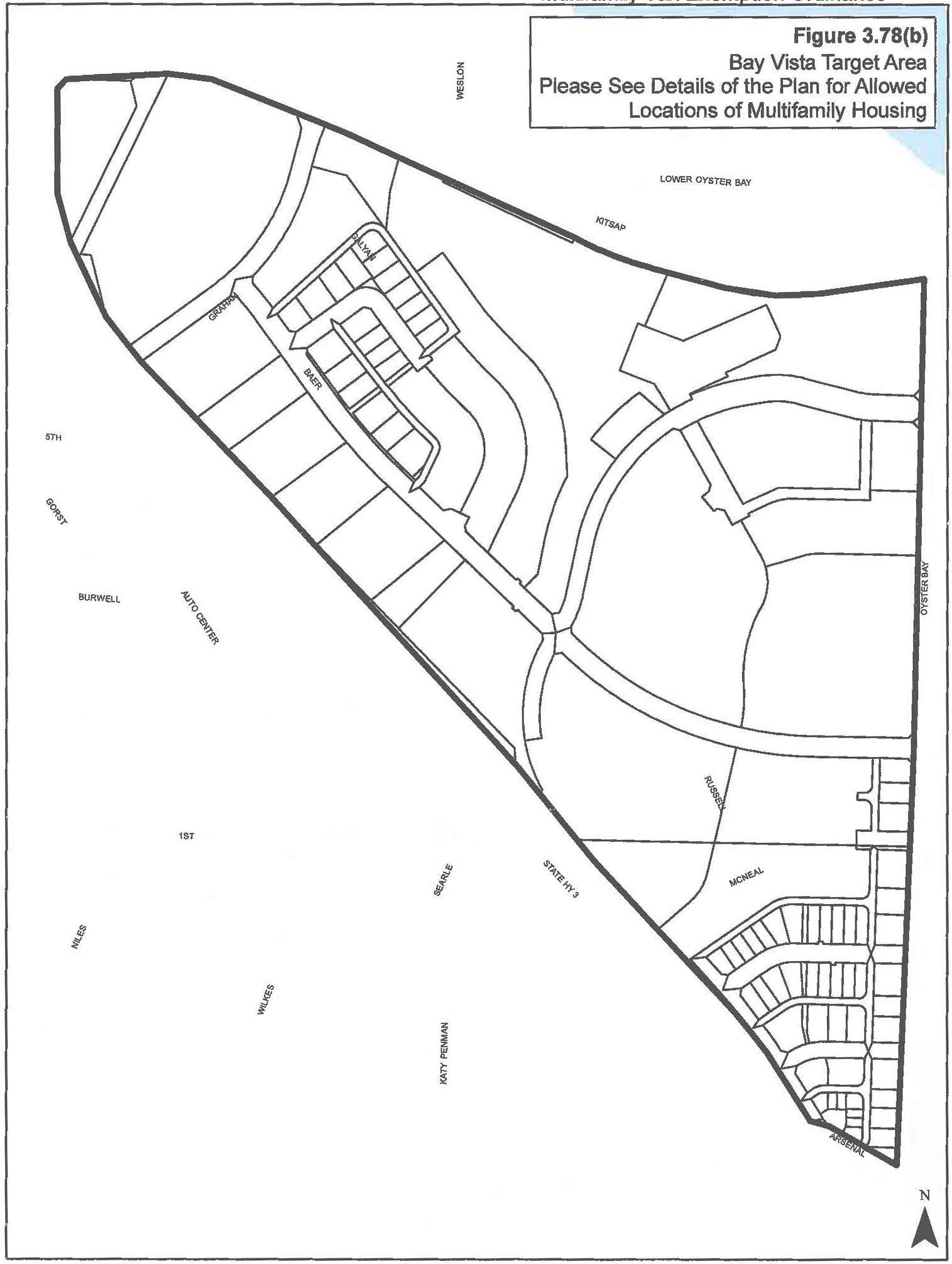

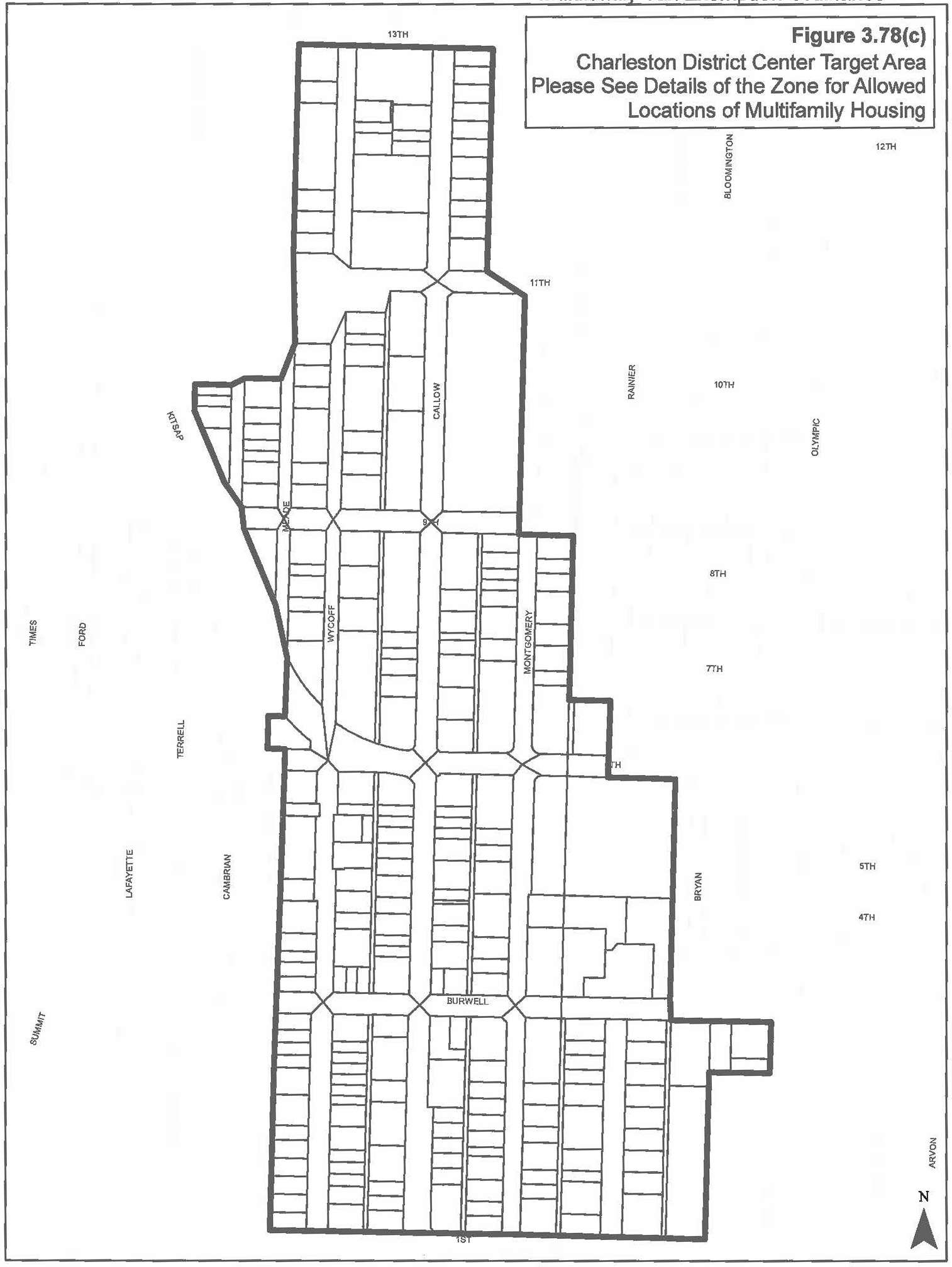

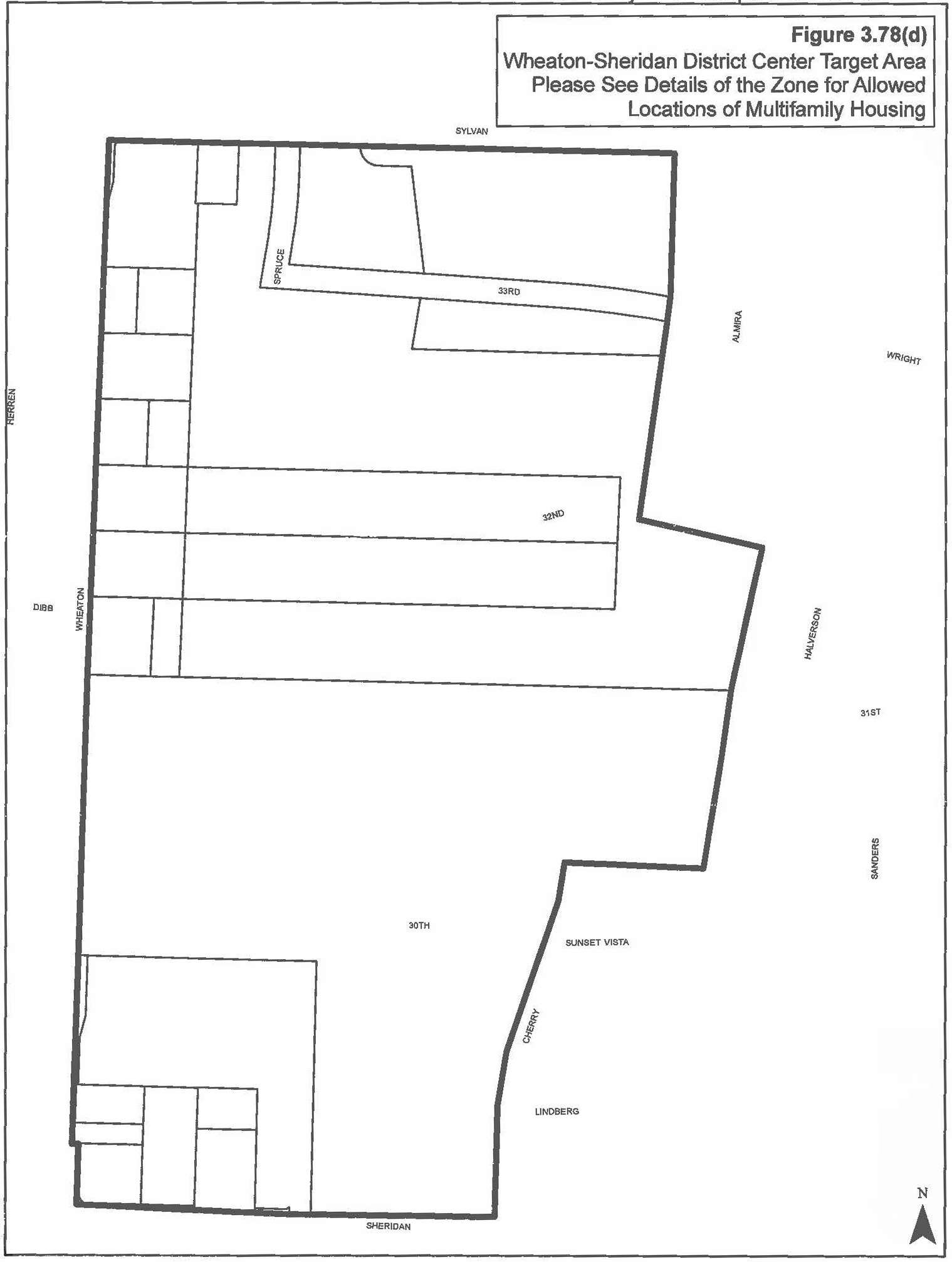

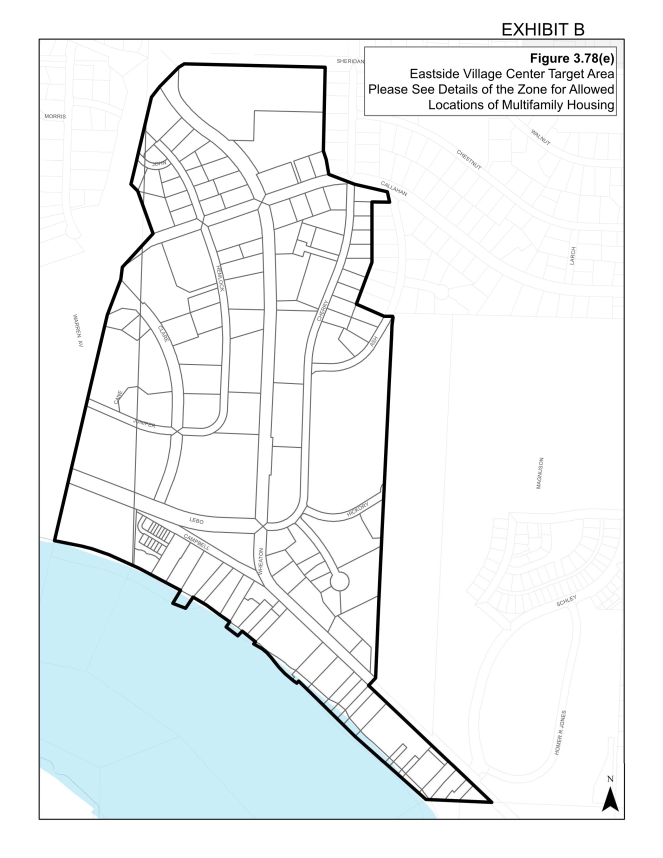

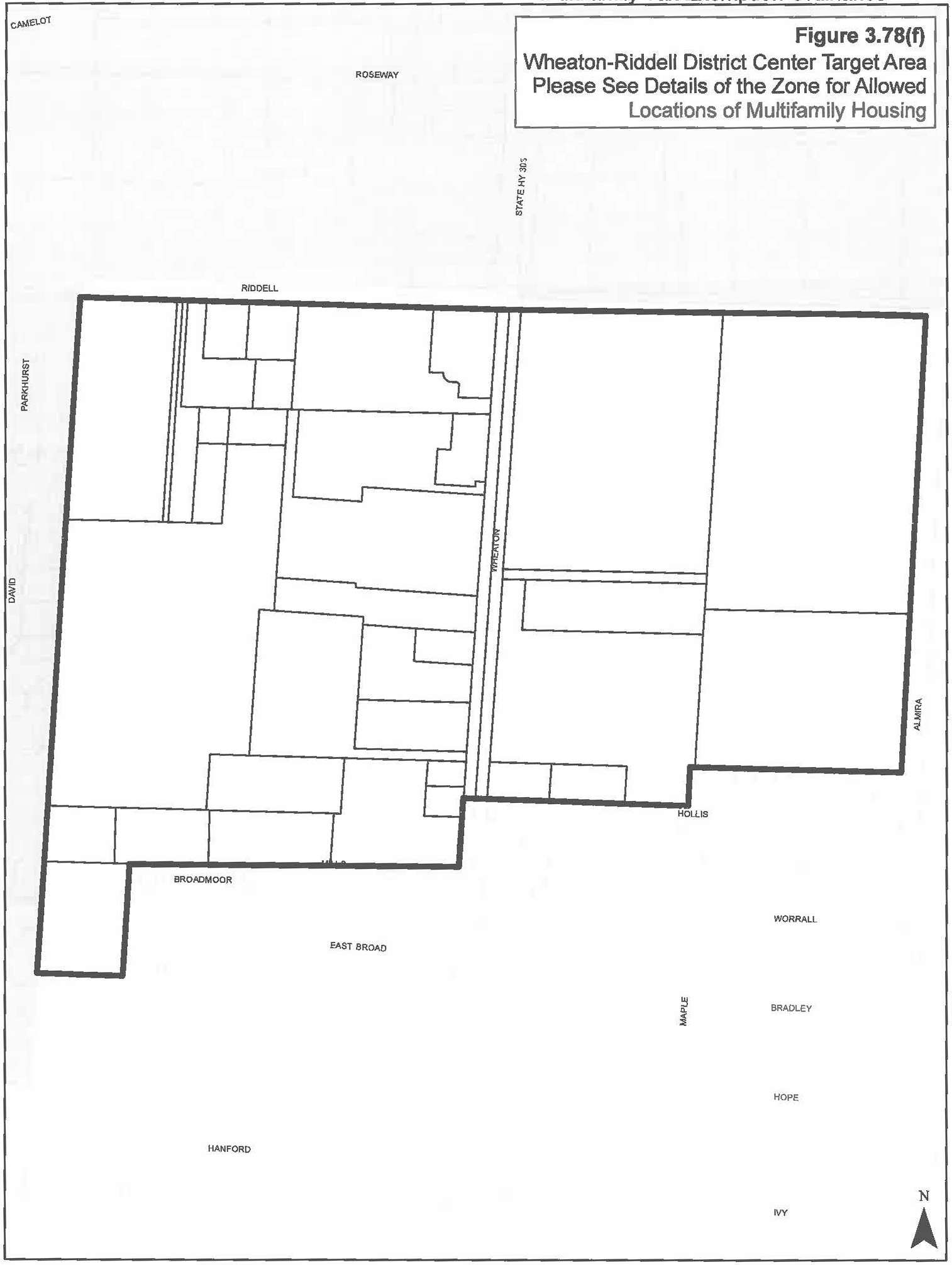

(n) "Residential targeted area," also "residential target area," means the geographic area located within the areas set forth in Figures 3.78(a) through 3.78(g).

(o) "Substantial compliance" means compliance with all local building, fire and zoning code requirements, which are typically required for rehabilitation as opposed to new construction. (Ord. 5463 §3, 2022; Ord. 5302 §4, 2016: Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.030 APPLICABILITY.

Multifamily housing projects in designated residential targeted areas resulting from new construction or rehabilitation or conversion of vacant, underutilized, or substandard buildings may be entitled to a limited exemption from ad valorem property taxation as set forth in this chapter. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.040 TERMS OF THE TAX EXEMPTION.

(a) Duration of Exemption. The value of new housing construction, conversion, and rehabilitation improvements qualifying under this chapter is exempt from ad valorem property taxation, as follows:

(1) For eight (8) successive years beginning January 1st of the year immediately following the calendar year of issuance of the certificate; or

(2) For twelve (12) successive years beginning January 1st of the year immediately following the calendar year of issuance of the certificate, if the property otherwise qualifies for the exemption under this chapter and meets the conditions in this subsection (a)(2). For the property to qualify for the twelve (12) year exemption under this subsection, the applicant must commit to renting or selling at least twenty (20) percent of the multifamily housing units as affordable housing units to low- and moderate-income households, and the property must satisfy that commitment and any additional affordability and income eligibility conditions adopted by the local government under this chapter. In the case of projects intended exclusively for owner occupancy, the minimum requirement of this subsection (a)(2) may be satisfied solely through housing affordable to moderate-income households. Low- and moderate-income household units shall be dispersed throughout the development and be apportioned among all unit types (i.e., studio, single bedroom, double bedroom, etc.) based on the number of each unit type to the extent feasible.

(3) For twenty (20) successive years beginning January 1st of the year immediately following the calendar year of issuance of the certificate, if the property otherwise qualifies for the exemption under this chapter and meets the conditions in this subsection (a)(3). To qualify for the exemption under this subsection, the applicant must commit to renting at least twenty (20) percent of the dwelling units as affordable to low- and moderate-income households for a term of at least ninety-nine (99) years, and the property must satisfy that commitment and all required affordability and income eligibility conditions adopted by the City under this chapter. The applicant shall record a covenant or deed restriction that ensures the continuing rental of units subject to these affordability requirements consistent with the conditions in this subsection (a)(3) for a period of no less than ninety-nine (99) years. The covenant or deed restriction must also address criteria and policies to maintain public benefit if the property is converted to a use other than that which continues to provide for permanently affordable low- and moderate-income households consistent with this subsection (a)(3). Low- and moderate-income household units shall be dispersed throughout the development and be apportioned among all unit types (i.e., studio, single bedroom, double bedroom, etc.) based on the number of each unit type to the extent feasible.

(b) Limits on Exemption. The exemption does not apply:

(1) To the value of land or to the value of nonhousing-related improvements not qualifying under this chapter.

(2) In the case of rehabilitation of existing buildings, to the value of improvements constructed prior to submission of the completed application required under this chapter.

(3) To increases in assessed valuation made by the Kitsap County Assessor on nonqualifying portions of building or other improvements and value of land nor to increases made by lawful order of a County board of equalization, the Department of Revenue, or Kitsap County, to a class of property throughout the County or specific area of the County to achieve the uniformity of assessment or appraisal required by law.

(c) Conclusion of Exemption. At the conclusion of the exemption period, the new or rehabilitated housing cost shall be considered as new construction for the purposes of Chapter 84.55 RCW. (Ord. 5463 §4, 2022; Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.050 PROJECT ELIGIBILITY.

A proposed multifamily housing project must meet the following requirements for consideration for a property tax exemption:

(a) Location. The project must be located within a residential targeted area as defined in BMC 3.78.020 and as set forth in Figures 3.78(a) through 3.78(g).

(b) Tenant Displacement Prohibited. The project must not displace existing residential tenants of structures that are proposed for redevelopment. If the property proposed to be rehabilitated is not vacant, an applicant shall provide each existing tenant housing of comparable size, quality, and price and a reasonable opportunity to relocate.

(1) General Notification. The applicant shall provide each displaced household at least twelve (12) months’ moving notice, unless mutually agreed otherwise by household and applicant.

(2) Relocation Assistance. Low-income households shall be provided the following:

(i) Assistance in securing housing of comparable size, quality, and price which meets Housing and Urban Development’s Uniform Physical Condition Standards or a similar standard acceptable to the City; and

(ii) First and last month expenses at the new housing location as defined above, and moving and relocating expenses as defined by the Department of Transportation Fixed Residential Moving Costs Schedule.

(c) Noncompliance with Building Codes. Existing dwelling units proposed for rehabilitation must fail to comply with one or more standards of the applicable state or City building codes.

(d) Size of Project. The new, converted, or rehabilitated multiple-unit housing must provide for a minimum of fifty (50) percent of the space for permanent residential occupancy. The project, whether new, converted, or rehabilitated multiple-unit housing, must include at least ten (10) units of multifamily housing within a residential structure or as part of an urban development. In the case of existing multifamily housing that is occupied or which has not been vacant for twelve (12) months or more, the multifamily housing project must also provide for a minimum of four (4) additional multifamily units for a total project of at least ten (10) units including the four (4) additional units. Existing multifamily housing that has been vacant for twelve (12) months or more does not have to provide additional units.

(e) Proposed Completion Date. New construction of multifamily housing and rehabilitation improvements must be completed within three (3) years from the date of approval of the application.

(f) Compliance with Guidelines and Standards. The project must be designed to comply with the City’s Comprehensive Plan, building, housing, and zoning codes, and any other applicable regulations. The project must also comply with any other standards and guidelines adopted by the City Council for the residential targeted area. (Ord. 5463 §5, 2022; Ord. 5302 §5, 2016: Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.060 APPLICATION PROCEDURE.

A property owner who wishes to propose a project for a tax exemption shall complete the following procedures:

(a) The application provided by the City shall be filed with the Department along with the required fees as established pursuant to RCW 84.14.080.

(b) A complete application shall include:

(1) A completed City of Bremerton application form setting forth the grounds for the exemption.

(2) Preliminary floor and site plans of the proposed project.

(3) A statement acknowledging the potential tax liability when the project ceases to be eligible under this chapter.

(4) An affidavit stating the occupancy record of the property for a period of twelve (12) months prior to filing the application.

(5) Verification by oath or affirmation of the information submitted.

(6) For rehabilitation projects, the applicant shall provide a report prepared by a registered architect identifying property noncompliance with the building codes. This report shall identify specific code violations and must include supporting data that satisfactorily explains and proves the presence of a violation. Supporting data must include a narrative and such graphic materials as needed to support this application. Graphic materials may include, but are not limited to, building plans, building details, and photographs. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.070 APPLICATION FOR CONDITIONAL CERTIFICATE.

The Director may certify as eligible an application which is determined to comply with the requirements of this chapter. A decision to approve or deny an application shall be made within ninety (90) calendar days of receipt of a complete application.

(a) Application. The Director may approve the application if he/she finds that:

(1) A minimum of ten (10) new units are being constructed or in the case of occupied rehabilitation or conversion within twelve (12) months of occupancy, a minimum of four (4) additional multifamily units for a total project of at least ten (10) units including the four (4) additional multifamily units are being developed.

(2) The proposed project is or will be, at the time of completion, in conformance with all applicable local plans and regulations.

(3) The owner has complied with all standards and guidelines adopted by the City under this chapter.

(4) The site is located in the residential targeted area.

(5) The proposed multiunit housing project meets the affordable housing requirements as described in BMC 3.78.040.

(b) Approval of Application. If an application is approved, the applicant shall enter into a contract with the City, regarding the terms and conditions of implementation of the project, and the Director shall issue a conditional certificate of acceptance of tax exemption. The conditional certificate shall expire three (3) years from the date of approval unless an extension is granted as provided in this chapter.

(c) Denial of Application. If an application is denied, the Director shall state in writing the reasons for denial and shall send notice to the applicant at the applicant’s last known address within ten (10) calendar days of the denial.

(d) Appeal. Per RCW 84.14.070, an applicant may appeal a denial to the City Council within thirty (30) calendar days of receipt of the denial by filing a complete appeal application and fee with the Director. The appeal before the City Council will be based on the record made before the Director. The Director’s decision will be upheld unless the applicant can show that there is no substantial evidence on the record to support the Director’s decision. The City Council’s decision on appeal will be final. (Ord. 5463 §6, 2022; Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.080 EXTENSION OF CONDITIONAL CERTIFICATE.

(a) Extension. The conditional certificate and time for completion of the project may be extended by the Director for a period not to exceed a total of twenty-four (24) consecutive months. To obtain an extension, the applicant must submit a written request with a fee stating the grounds for the extension. An extension may be granted if the Director determines that:

(1) The anticipated failure to complete construction or rehabilitation within the required time period is due to circumstances beyond the control of the owner;

(2) The owner has been acting and could reasonably be expected to continue to act in good faith and with due diligence; and

(3) All the conditions of the original contract between the applicant and the City will be satisfied upon completion of the project.

(b) Denial of Extension. If an extension is denied, the Director shall state in writing the reason for denial and shall send notice to the applicant’s last known address within ten (10) calendar days of the denial.

(c) Appeal. Pursuant to RCW 84.14.090(6), an applicant may appeal the denial of an extension to the Hearing Examiner pursuant to Chapter 2.13 BMC within fourteen (14) calendar days of receipt of the denial by filing a complete appeal application and fee with the Director. The appeal before the Hearing Examiner shall be processed as a Type I Director decision pursuant to Chapter 20.02 BMC. No appeal to the City Council is provided from the Hearing Examiner’s decision. The applicant may appeal the Hearing Examiner’s decision to the Kitsap County Superior Court, under RCW 34.05.510 through 34.05.598, if the appeal is filed within thirty (30) calendar days of receiving notice of that decision. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.090 APPLICATION FOR FINAL CERTIFICATE.

Upon completion of the improvements agreed upon in the contract between the applicant and the City and upon issuance of a certificate of occupancy, the applicant may request a final certificate of tax exemption by filing with the Director the following:

(a) A statement of expenditures made with respect to each multifamily housing unit and the total expenditures made with respect to the entire property;

(b) A description of the completed work and a statement of qualification for the exemption;

(c) A statement that the work was completed within the required three (3) year period or any authorized extension; and

(d) If applicable, that the project meets the affordable housing requirements as described in RCW 84.14.020. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.100 ISSUANCE OF FINAL CERTIFICATE.

Within thirty (30) calendar days of receipt of all materials required for a final certificate, the Director shall determine whether the specific improvements satisfy the requirements of the contract, application, and this chapter.

(a) Granting of Final Certificate. If the Director determines that the project has been completed in accordance with this chapter and the contract between the applicant and the City, and has been completed within the authorized time period, the City shall, within ten (10) calendar days of the expiration of the thirty (30) day review period above, file a final certificate of tax exemption with the Kitsap County Assessor.

(b) Denial of Final Certificate. The Director shall notify the applicant in writing that a final certificate will not be filed if the Director determines that:

(1) The improvements were not completed within the authorized time period;

(2) The improvements were not completed in accordance with the contract between the applicant and the City; or

(3) The owner’s property is otherwise not qualified under this chapter.

(c) Appeal. Pursuant to RCW 84.14.090(6), an applicant may appeal a denial to the Hearing Examiner pursuant to Chapter 2.13 BMC within fourteen (14) calendar days of issuance of the denial of a final certificate by filing a complete appeal application and fee with the Director. The appeal before the Hearing Examiner shall be processed as a Type I Director decision pursuant to Chapter 20.02 BMC. No appeal to the City Council is provided from the Hearing Examiner’s decision. The applicant may appeal the Hearing Examiner’s decision to the Kitsap County Superior Court, under RCW 34.05.510 through 34.05.598, if the appeal is filed within thirty (30) calendar days of receiving notice of that decision. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.105 AFFORDABLE HOUSING CAPITAL FUND.

If an application for the multifamily tax exemption is approved, the project has completed construction, and a final certificate of property tax exemption has been issued as set forth in BMC 3.78.100, the Director of Financial Services, or designee, shall transfer to the affordable housing capital fund revenues based on the anticipated sales tax received or to be received by the City for the construction of the project. The Director shall determine the value of the sales tax revenues to be transferred to the fund based on (1) the City’s portion of the current sales tax rate for the construction, and (2) the estimated cost of construction as established in the building permit application and other relevant information as the Director deems appropriate. Once established, the funds will be transferred to the affordable housing capital fund at the beginning of the next fiscal year. The funds shall be used for affordable housing projects approved by the City Council, unless the funds are otherwise allocated by the City Council. (Ord. 5353 §2, 2018)

3.78.110 ANNUAL COMPLIANCE REVIEW.

(a) Within thirty (30) calendar days after the first anniversary of the date of filing the final certificate of tax exemption and each year for the tax exemption period, the property owner shall be required to file a notarized declaration with the Director indicating the following:

(1) A statement of occupancy and vacancy of the multifamily units during the previous twelve (12) months;

(2) A certification by the owner that the property has not changed use and, if applicable, that the property has been in compliance with the affordable housing requirements as described in RCW 84.14.020 since the date of the certificate approved by the City;

(3) A description of changes or improvements constructed after issuance of the certificate of tax exemption; and

(4) Any information needed by the City to file its report pursuant to subsection (b) of this section and any additional information requested by the City in regards to the units receiving a tax exemption.

(b) The City shall report annually consistent with requirements as described in RCW 84.14.100 to the Washington State Department of Commerce. The report must include the following information, or as otherwise required per Chapter 84.14 RCW:

(1) The number of tax exemption certificates granted;

(2) The total number and type of units produced or to be produced;

(3) The number and type of units produced or to be produced meeting affordable housing requirements;

(4) The actual development cost of each unit produced;

(5) The total monthly rent or total sale amount of each unit produced;

(6) The income of each renter household at the time of initial occupancy and the income of each initial purchaser of owner-occupied units at the time of purchase for each of the units receiving a tax exemption and a summary of these figures for the City; and

(7) The value of the tax exemption for each project receiving a tax exemption and the total value of tax exemptions granted.

(c) City staff may also conduct on-site verification of the declaration. Failure to submit the annual declaration shall result in a review of the exemption per RCW 84.14.110. (Ord. 5463 §7, 2022; Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.120 CANCELLATION OF TAX EXEMPTION.

If the Director determines the owner is not complying with the terms of the contract or this chapter, the tax exemption shall be canceled. This cancellation may occur in conjunction with the annual review or at any other time when noncompliance has been determined. If the owner intends to convert the multifamily housing to another use, the owner shall notify the Director and the Kitsap County Assessor in writing within sixty (60) calendar days of the change in use.

(a) Effect of Cancellation. If a tax exemption is canceled due to a change in use or other noncompliance, the following taxes and penalties will apply:

(1) Additional real property tax, plus interest, shall be imposed based upon the value of the nonqualifying improvements. This additional tax is calculated based upon the difference between the property tax paid and the property tax that would have been paid if it had included the value of the nonqualifying improvements dated back to the date that the improvements were converted to a nonqualifying use.

(2) A penalty shall be imposed amounting to twenty (20) percent of the value of the additional property tax plus interest.

(3) The interest is calculated at the same statutory rate charged on delinquent property taxes from the dates on which the additional property tax could have been paid without penalty if the improvements had been assessed at full value without regard to this tax exemption program.

(4) The additional taxes, interest and penalties will become a lien on the land and attach at the time the property or portion of the property is removed from multifamily use or the amenities no longer meet applicable requirements. The lien has priority over and must be fully paid and satisfied before a recognizance, mortgage, judgment, debt, obligation, or responsibility to or with which the land may become charged or liable. The lien may be foreclosed upon expiration of the same period after delinquency and in the same manner provided by law for foreclosure of liens for delinquent real property taxes. An additional tax unpaid on its due date is delinquent. From the date of delinquency until paid, interest must be charged at the same rate applied by law to delinquent ad valorem property taxes.

(b) Notice of Cancellation. Pursuant to RCW 84.14.110(2), upon determining that a tax exemption is to be canceled, the Director shall notify the owner by mail, return receipt requested.

(c) Appeal. The property owner may appeal the determination of cancellation of the tax exemption to the Hearing Examiner pursuant to Chapter 2.13 BMC by filing a notice of appeal with the City Clerk within thirty (30) calendar days, specifying the factual and legal basis for the appeal. The Hearing Examiner will conduct a hearing under Chapter 20.02 BMC for a Process I action. An aggrieved party may appeal the Hearing Examiner’s decision to the Kitsap County Superior Court under RCW 34.05.510 through 34.05.598. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.130 CONFLICT OF PROVISIONS.

If any provision of this chapter is in legal conflict with the provisions of Chapter 84.14 RCW, the provisions of Chapter 84.14 RCW shall apply as if set forth in this chapter. (Ord. 5036 §1 (part), 2007: Ord. 4968 §1 (part), 2006)

3.78.140 EXTENSION OF TAX EXEMPTION.

Pursuant to RCW 84.14.020(6), the Administrator may approve an extended exemption of the project that qualified for, satisfied the conditions of, and utilized the exemption as provided in subsection (a)(2) of this section from ad valorem property taxation for up to a total of twelve (12) successive years beginning January 1st of the year immediately following the calendar year that the original exemption expires.

(a) The owner of property applying for extended exemption under this subsection shall submit an application to the Administrator on a form established by the Administrator. The owner shall verify the correctness of the information contained in the application by his/her signature and affirmation made under penalty of perjury under the laws of the State of Washington. The application shall contain such information as the Administrator may deem necessary or useful, which at a minimum shall include:

(1) A statement from the owner acknowledging the potential tax liability when the property ceases to be eligible for exemption, equivalent to BMC 3.78.060; and

(2) Information required for the final exemption certificate pursuant to BMC 3.78.100; and

(3) Information required for the annual report pursuant to BMC 3.78.110.

(b) Deadline. The extension application shall be submitted to the Administrator no later than August 31st of the year the original exemption expires. (Ord. 5463 §8, 2022)

(Ord. 5302 §3 (Exh. B) (part), 2016)

(Ord. 5302 §3 (Exh. B) (part), 2016)

(Ord. 5302 §3 (Exh. B) (part), 2016)

(Ord. 5302 §3 (Exh. B) (part), 2016)

(Ord. 5463 §9, 2022)

(Ord. 5302 §3 (Exh. B) (part), 2016)

(Ord. 5302 §3 (Exh. B) (part), 2016)